Introduction

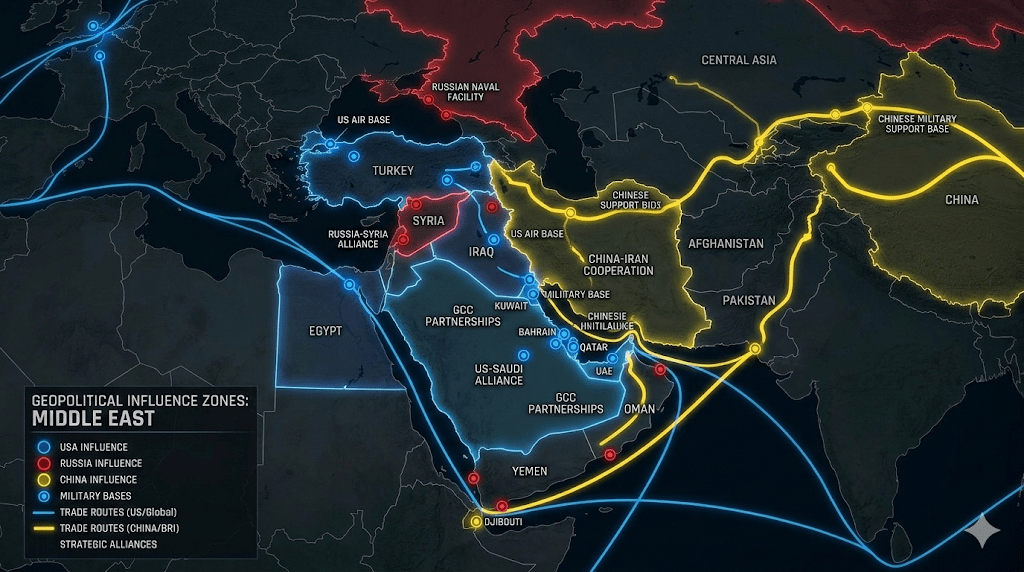

Even amid de-escalation signals in the Middle East, one structural vulnerability remains unchanged: the Strait of Hormuz.

Roughly a fifth of global oil flows through this narrow waterway, making it one of the most critical chokepoints in the global energy system.

In 2026, the question is not whether disruption will occur—but how markets price the risk of it.

H2: A Strategic Chokepoint

The Strait connects major producers to global markets.

Its importance lies in:

- high concentration of oil shipments

- limited alternative routes

- geopolitical sensitivity

Even temporary disruptions can have immediate global consequences.

H2: Why Markets React Instantly

Energy markets are highly sensitive to signals from the region.

Even without actual disruption:

👉 perceived risk increases

👉 insurance and shipping costs rise

👉 prices adjust upward

This is the mechanism of risk pricing in action.

H2: LNG and Shipping Exposure

The Strait is not only about oil.

LNG shipments from the Gulf also depend on safe passage.

This creates exposure for:

- Europe

- Asian importers

- global energy traders

Any instability affects both oil and gas markets simultaneously.

H2: Europe’s Indirect Vulnerability

Europe is geographically distant—but economically exposed.

Higher oil and LNG prices translate into:

- increased import costs

- inflationary pressure

- industrial strain

This reinforces Europe’s position as a price-taker.

H2: Can the Risk Be Reduced?

Efforts to mitigate risk include:

- diversification of supply

- strategic reserves

- alternative infrastructure

But geography cannot be changed.

The Strait remains a fixed vulnerability in a globalized system.

Conclusion

The Strait of Hormuz is more than a geographic feature—it is a structural risk embedded in global energy markets.

Even in periods of relative calm, its influence persists.

In 2026, stability depends not only on supply—but on the uninterrupted flow through a narrow passage.

FAQ

Q1: Why is the Strait of Hormuz important?

It carries a large share of global oil and gas shipments.

Q2: Can tensions affect prices without disruption?

Yes, through increased risk perception.

Q3: Does Europe depend on it?

Indirectly, through global pricing.

Q4: Can the risk be eliminated?

No, only managed.